Understanding the difference between GSTR-1 and GSTR-3B is essential for every GST-registered business in India. Although both returns are mandatory, many taxpayers confuse their purpose, filing structure, and due dates. As a result, errors occur, leading to notices, penalties, or reconciliation issues.

Therefore, in this detailed guide, we will explain the key differences between GSTR-1 and GSTR-3B, their filing process, due dates, and common mistakes to avoid.

If you prefer professional assistance instead of handling compliance alone, you can rely on our trusted GST Return Filing Services in India for accurate and timely filing.

What is GSTR-1?

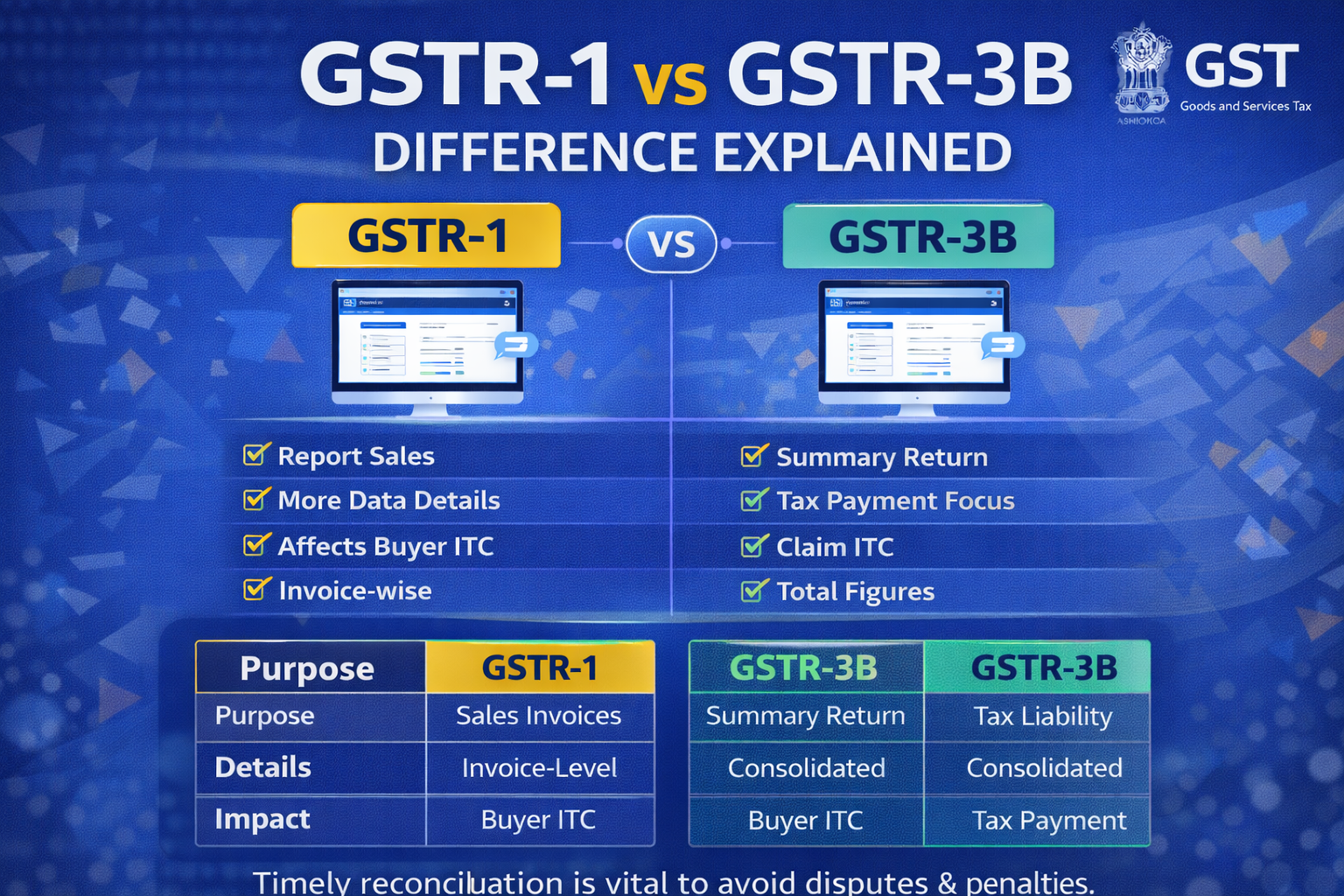

First and foremost, GSTR-1 is a return that contains details of outward supplies (sales). Every registered taxpayer must report invoice-wise details of sales made during the tax period.

Key Features of GSTR-1:

- Contains B2B and B2C sales details

- Includes export invoices (if applicable)

- Updates buyer’s GSTR-2A / 2B

- Filed monthly or quarterly

Consequently, accuracy in GSTR-1 directly affects your customer’s ITC claim.

What is GSTR-3B?

On the other hand, GSTR-3B is a summary return. It does not require invoice-wise details but instead captures total tax liability and eligible Input Tax Credit.

Key Features of GSTR-3B:

- Summary of sales and purchases

- ITC claimed

- Tax payable

- Self-declaration based

Therefore, while GSTR-1 reports detailed sales, GSTR-3B focuses on tax payment.

Major Differences Between GSTR-1 and GSTR-3B

| Basis | GSTR-1 | GSTR-3B |

|---|---|---|

| Purpose | Report sales invoices | Summary of tax liability |

| Details | Invoice-level data | Consolidated figures |

| Impact | Affects buyer ITC | Determines tax payment |

| Frequency | Monthly/Quarterly | Monthly |

Thus, both returns serve different but interconnected purposes.

Why Matching GSTR-1 and GSTR-3B is Important

Although both returns are separate, they must match logically. If sales declared in GSTR-1 do not align with tax declared in GSTR-3B, discrepancies arise.

Consequently:

- Notices may be issued

- ITC may be blocked

- Additional tax liability may arise

Therefore, reconciliation before filing is critical.

Filing Process for GSTR-1

Step 1: Login to GST portal

Step 2: Select return period

Step 3: Enter B2B invoices

Step 4: Enter B2C sales

Step 5: Validate and submit

Step 6: File using EVC/DSC

However, invoice errors can create ITC mismatches for customers. Hence, double-checking is essential.

Filing Process for GSTR-3B

Step 1: Select GSTR-3B

Step 2: Enter outward supplies summary

Step 3: Enter ITC details

Step 4: Calculate tax liability

Step 5: Offset liability

Step 6: Submit and file

Although simpler than GSTR-1, incorrect tax reporting can lead to interest and penalties.

Due Dates for GSTR-1 and GSTR-3B

Generally:

- GSTR-1 → 11th of next month

- GSTR-3B → 20th of next month

However, quarterly filers under QRMP scheme have different timelines.

Therefore, keeping track of due dates is extremely important.

You can also read about GST return due dates 2026 to avoid late filing penalties.

Common Mistakes Businesses Make

Even experienced taxpayers sometimes make errors such as:

- Filing GSTR-3B without reconciling GSTR-1

- Claiming excess ITC

- Missing invoices

- Reporting incorrect tax rates

- Delayed filing

As a result, penalties and notices may follow.

To avoid such risks, many businesses choose professional GST Return Filing Services in India to ensure proper reconciliation and compliance.

Late Filing Consequences

If either GSTR-1 or GSTR-3B is delayed:

- ₹50 per day late fee

- ₹20 per day for Nil returns

- 18% annual interest on unpaid tax

- E-way bill blockage

Consequently, timely filing protects both financial and operational stability.

Practical Compliance Tips

Instead of waiting until the last date:

- Maintain real-time bookkeeping

- Reconcile sales and purchases monthly

- Cross-check ITC before filing

- Keep sufficient balance for tax payment

- Review data carefully before submission

In addition, using accounting software reduces manual errors.

Should You File Returns Yourself?

While small businesses may attempt self-filing, growing businesses often face:

- High transaction volume

- Multi-state operations

- Complex ITC reconciliation

- Frequent compliance updates

Therefore, outsourcing compliance often saves time and prevents costly errors.

Frequently Asked Questions

1. Is GSTR-1 mandatory if there are no sales?

Yes, Nil return must be filed.

2. Can GSTR-3B be revised?

No, corrections must be made in subsequent returns.

3. What happens if GSTR-1 and GSTR-3B mismatch?

The GST department may issue notices seeking clarification.

Final Thoughts

To summarize, GSTR-1 and GSTR-3B are both essential components of GST compliance. Although they serve different purposes, they must be aligned and filed accurately to avoid penalties.

Moreover, reconciliation between invoice-level data and summary tax liability is crucial for smooth compliance.

Instead of risking errors or missing deadlines, you can rely on experienced professionals for accurate and timely filing.

If you need expert assistance, connect with us for reliable GST Return Filing Services in India today.

📞 Talk to a GST Expert

💬 WhatsApp for Instant Support

🌐 Visit: https://accountingfirm4u.com/